Pastis Expands to West Palm Beach, Joining the Trendy Nora District

In a move that further cements South Florida's status as a burgeoning culinary hotspot, renowned New York bistro Pastis is set to open its fourth U.S. location in West Palm…

In a move that further cements South Florida's status as a burgeoning culinary hotspot, renowned New York bistro Pastis is set to open its fourth U.S. location in West Palm…

The Big Apple's real estate market is witnessing a shift as Manhattan's rental landscape evolves and home sales gain momentum. Recent data from Douglas Elliman, analyzed by Miller Samuel, reveals…

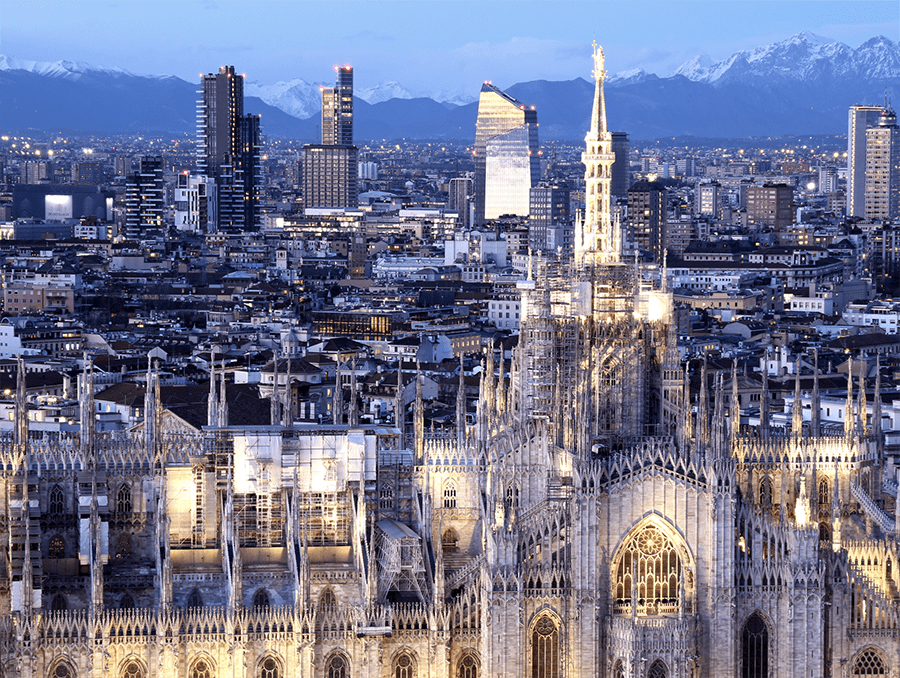

In a surprising turn of events, Italy's real estate market is showing signs of life after six consecutive quarters of decline. However, Milan, the country's financial powerhouse, finds itself swimming…

In a move that underscores the evolving dynamics of New York City's commercial real estate market, Nasdaq is set to vacate its former Times Square headquarters at 1500 Broadway. This…

New York City's iconic Madison Avenue, long synonymous with high-end retail and opulent shopping experiences, is on the brink of a dramatic transformation. The stretch where East Midtown meets the…

In a move that epitomizes the shifting tides of financial power, hedge fund titan Ken Griffin is doubling down on his Florida gambit with an ambitious plan for Citadel's new…

In a significant shift for one of New York City’s architectural icons, the Flatiron Building is set to undergo a residential transformation spearheaded by The Brodsky Organization. Nearly a year…

In a bold move that could reshape Manhattan's skyline and real estate market, New York's most ambitious office-to-residential conversion project is breaking ground. The former Pfizer headquarters near Grand Central…

In a surprising twist of real estate dynamics, Florida residents are increasingly trading their sun-soaked paradises for the concrete jungle of New York City. This trend, emerging as a counterpoint…

Renowned for its dedication to the Neapolitan sartorial tradition, Amina Rubinacci, the womenswear brand beloved by tourists on Capri and the Amalfi Coast, is making a significant leap into the…